You log into your banking app, scroll past the checking balance, and there they are the numbers that make your stomach tighten. Maybe it is a lingering student loan, a credit card balance from an emergency car repair, or a holiday that cost more than it should have. If you are watching a chunk of your hard-earned salary evaporate into interest fees every single month, you are not alone, and you do not have to stay trapped.

Living with debt has become a structural reality for our generation. Across North America, Europe, and emerging economic hubs worldwide, central banks have held interest rates higher for longer to combat inflation. This means the variable interest rate on your credit card has likely crept up to 21% or higher, and personal loans are more expensive than they have been in fifteen years. In this macroeconomic climate, standard money management is no longer just about budgeting; it is about aggressive financial self-defense. Leaving your debt to simmer on minimum payments is a guaranteed way to overpay for your past while sacrificing your future wealth. To take control of your personal finance journey, you need a strategy optimized for pure efficiency. That strategy is the Debt Avalanche.

1. Understand the Mechanics of the Avalanche

The Avalanche Method is a debt payoff strategy where you list all your debts from the highest interest rate to the lowest interest rate, regardless of the balance size. You commit to making the minimum required payments on every single debt to keep your accounts in good standing and protect your credit score. Then, you throw every extra spare dollar, euro, or franc you can find at the debt with the absolute highest interest rate. Once that top card or loan is fully wiped out, you take its entire monthly payment the minimum plus the extra cash and avalanche it down directly into the next highest interest rate debt on your list.

2. Appreciate the Mathematical Victory

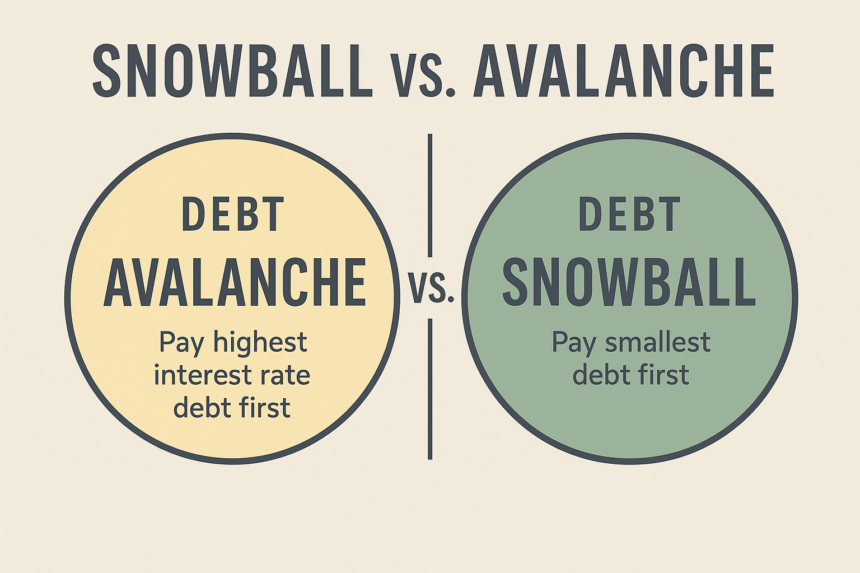

Why choose this over other popular money management strategies like the Debt Snowball? The answer comes down to pure, unvarnished mathematics. The Snowball method focuses on behavior, targeting the smallest balances first to give you quick psychological wins. The Avalanche, by contrast, focuses entirely on minimizing your lifetime interest expenses. By eliminating the most expensive debt first, you stop compounding interest from working against you. You save the maximum amount of money possible on interest payments, and you shorten your total timeline to becoming completely debt-free.

Case Study: The Avalanche in Action Let’s look at a realistic scenario for a mid-career professional carrying three distinct liabilities. Imagine you have a total debt load of $22,000 distributed across three different financial products:

- Credit Card A: $4,000 balance at 24% APR (Minimum payment: $120)

- Personal Loan B: $10,000 balance at 12% APR (Minimum payment: $250)

- Student Loan C: $8,000 balance at 6% APR (Minimum payment: $100)

Under the Avalanche system, your target sequence is explicitly locked: Credit Card A (24%), then Personal Loan B (12%), and finally Student Loan C (6%). You pay the base total of $470 across all three just to stay current. But let’s assume you audit your monthly spending and find an extra $300 to accelerate your path to freedom.

3. Direct Your Financial Firepower

With an extra $300 available, your total monthly debt payoff budget becomes $770. You continue to pay the $250 minimum for Personal Loan B and the $100 minimum for Student Loan C. However, you combine your remaining $120 minimum for Credit Card A with your extra $300, sending a massive $420 payment to that 24% card every single month. Instead of watching that $4,000 balance drag on for years while accumulating hundreds of dollars in high-interest fees, you will utterly incinerate the principal balance in roughly ten months.

4. Execute the Momentum Shift

This is where the avalanche effect truly earns its name. The moment Credit Card A hits a zero balance, you do not take that $420 and spend it on a weekend away or a new wardrobe. Instead, you redirect that entire sum to your next target: Personal Loan B. You were already paying the $250 minimum on that loan. Now, you add the $420 you used to send to the credit card, creating a powerhouse monthly payment of $670. Because you are attacking a 12% loan with such heavy volume, the principal drops rapidly, cutting years off the loan term. By the time you reach your final debt the 6% student loan your payment swells to a massive $770 per month. You are using the exact same total out-of-pocket monthly budget you started with, but your impact has multiplied.

5. Audit and Automate Your Cash Flow

To make this system work without relying on pure willpower every month, you must build an automated infrastructure. Start by logging into your online banking accounts and setting up automatic payments for all your minimum amounts. This guarantees you will never suffer a late fee or a ding to your credit profile. Next, set up a recurring manual or automatic overpayment to your highest-interest target on the day you receive your salary. Treating your extra debt payment like an immediate, non-negotiable tax on your income ensures that you never accidentally spend your debt payoff fund on discretionary lifestyle purchases.

6. Stay Mindful of the Mental Game

While the mathematical benefits of this approach are indisputable, the Avalanche method does have one distinct vulnerability: patience. If your highest interest rate debt also happens to carry a massive balance, it might take months before you see a single account hit zero. During this initial phase, it can feel like you are throwing money into a black hole. When motivation flags, look at your interest savings instead of your balance reductions. Use a free online debt calculator to track how much future money you are saving from the banks. Remind yourself that every dollar of high-interest principal you eliminate is a guaranteed, tax-free return on your investment.

7. Keep Your Lifestyle in Check

The greatest threat to a successful debt payoff plan is lifestyle creep. As you watch your balances decline and your available mental bandwidth expand, it is incredibly easy to justify small upgrades to your daily spending. Guard against this trap fiercely. True financial freedom isn’t about looking wealthy; it is about owning your time and your income. Keep your living expenses locked down at their current level until your final target is entirely cleared. The short-term sacrifice will yield massive long-term flexibility.

Take Your First Step Today

Debt can feel like a heavy anchor holding your personal finance goals back, but it is ultimately just a math problem waiting to be solved. By using the Avalanche Method, you take control of the equation, ensuring that not a single cent of your money is wasted on unnecessary interest fees. You do not need to wait for a massive salary raise or a financial miracle to start changing your reality.